Commercial Real Estate Crisis: High Vacancy Rates Ahead

The commercial real estate crisis has emerged as a pressing concern in the wake of the pandemic, with soaring office vacancy rates raising alarms among economic analysts. In major cities like Boston, these rates have skyrocketed to between 12% and 23%, threatening to devalue properties and disrupt market stability. As many businesses adjust their work models, the reluctance of the Federal Reserve to lower interest rates further compounds the issue, potentially leading to significant losses for banks holding vast amounts of real estate loans. The looming maturity of commercial mortgage debt, with $4.7 trillion at risk, exacerbates banking system vulnerabilities, casting shadows of doubt over financial institutions still recovering from previous economic downturns. The implications of this crisis extend beyond real estate, potentially rippling through the economy and impacting consumers in ways that are yet to be fully understood.

As we delve deeper into the current dilemma facing commercial properties, it’s essential to consider the ramifications of high office vacancy levels and the rising cost of borrowing. This situation, often described as a real estate downturn, poses critical challenges for investors and the banking sector alike. With an influx of commercial mortgage debt approaching maturity, the strain on financial institutions raises questions about the overall health of the economy. Moreover, the repercussions of regional banking vulnerabilities become increasingly evident, affecting lending practices and consumer spending habits in various markets. Recognizing the economic implications of this predicament allows for a comprehensive understanding of its potential to influence broader financial conditions.

The Rising Threat of High Office Vacancy Rates

High office vacancy rates have become a pressing concern for urban economies, particularly as remote work persists. With cities like Boston reporting vacancy figures between 12 to 23 percent, the demand for traditional office spaces is plummeting. This significant decline in occupancy not only reflects changing work habits but also exerts downward pressure on property values. As buildings remain empty, businesses that rely on foot traffic and nearby patronage suffer, leading to broader economic implications for local economies that depend on vibrant commercial districts.

The impact of high office vacancy rates goes beyond immediate financial losses for property owners; it creates a ripple effect that can destabilize local economies. Local businesses, especially those catering to office workers, may face decreased sales, leading to layoffs and further economic slowdown. Additionally, a prolonged period of elevated vacancy rates can discourage new investments in the area, negatively impacting job creation and resulting in urban decay. As cities grapple with these challenges, the need for innovative solutions to repurpose unused office spaces becomes even more crucial.

Understanding the Impact of Interest Rates on Real Estate

Interest rates play a critical role in the health of the commercial real estate sector, influencing borrowing costs and investment strategies. With the Federal Reserve maintaining a cautious approach to interest rates, many real estate investors are feeling the pinch. Increased rates raise the cost of financing, and as a result, property developers and buyers are finding it more challenging to secure loans for new projects. This hesitance among investors can lead to slower developments and an imbalance in real estate supply and demand, further exacerbating high vacancy rates and leading to a broader commercial real estate crisis.

Moreover, the relationship between high interest rates and economic health is multifaceted. As rates rise, borrowing becomes more expensive not only for commercial projects but also for consumers looking to finance homes or businesses. This tightening can slow down economic activity, as individuals and companies may cut back on spending due to increased financial strain. In turn, this economic slowdown can lead to higher delinquency rates on loans, especially in the commercial real estate sector, creating further vulnerabilities within the banking system.

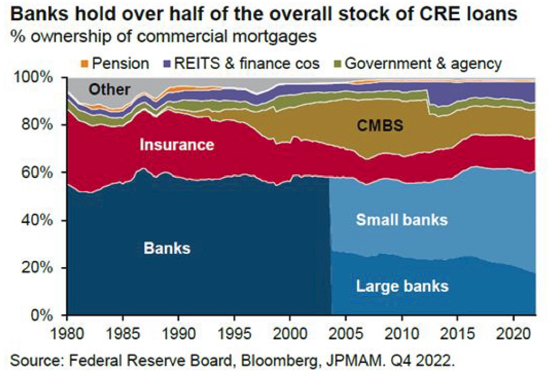

Banking System Vulnerabilities within Commercial Real Estate

The current landscape of banking reveals significant vulnerabilities, particularly concerning commercial real estate loans. With approximately 20 percent of commercial mortgage debt maturing this year, financial institutions could face substantial risks related to increased delinquency rates. Kenneth Rogoff, a noted expert on financial crises, highlights the danger this presents not just to individual banks but also to the broader financial system. If a substantial number of these loans become uncollectible, it could trigger a cascade effect that undermines the stability of regional banks, especially those heavily invested in real estate.

The reliability of smaller banks, which often lack the rigorous capital standards imposed on larger financial institutions, has come under scrutiny. While larger banks may be better positioned to absorb losses, many smaller entities could struggle, potentially leading to failures akin to those seen during the 2008 financial crisis. The interplay of high vacancy rates and the looming wave of loan maturities creates a precarious situation, necessitating close monitoring and potential interventions from regulatory bodies to prevent widespread disruptions.

Analyzing the Broader Economic Implications

The interconnectedness between commercial real estate and broader economic health cannot be overstated. As firms incur losses from their investments in commercial properties, and consumer confidence wanes in response to rising interest rates, the overall economic landscape may begin to shift. Stricter lending standards and reduced consumer spending could lead to economic stagnation or even recession, particularly if the commercial real estate crisis deepens.

However, it’s important to recognize that the current climate is not entirely bleak. Despite the challenges posed by high interest rates and vacancy rates, the U.S. economy as a whole is benefiting from a robust job market and strong stock performance. This juxtaposition indicates that while commercial real estate faces severe hurdles, the broader economic picture is more complex, with potential for resilience. Policymakers must tread carefully, balancing support for the commercial real estate sector without overextending resources that could exacerbate financial vulnerabilities.

The Role of Pension Funds in the Real Estate Crisis

Pension funds are significant players in the commercial real estate market, and their vulnerability to the impending crisis merits attention. Holding substantial amounts of capital in real estate investments, pension funds may face considerable losses should property values continue to decline—a trend already reflected in the heightened volumes of delinquent loans. Given the integral role that pension funds play in providing retirement security for millions, their potential exposure to a commercial real estate crisis carries implications that extend far beyond the financial sector.

As pension funds deal with potential downturns in real estate valuation, the associated impacts on retirees’ fortunes could prompt a reevaluation of investment strategies across the board. Institutions may pivot towards safer assets, limiting their engagement with commercial real estate and thereby exacerbating liquidity issues for an already beleaguered sector. This situation highlights the need for diversified investment approaches that can withstand fluctuations in market conditions while safeguarding the future financial stability of millions of retirees reliant on these funds.

Adaptations and Solutions to Preventing a Financial Crisis

To avert a protracted financial crisis stemming from the commercial real estate sector, many stakeholders are calling for strategic adaptations. One potential solution includes the repurposing of vacant office spaces into residential or mixed-use developments. By creatively addressing the issue of high vacancy rates, cities can revitalize underperforming areas, thus stimulating local economies. However, various logistical challenges remain, such as zoning laws and building codes, which must be navigated to facilitate such transformations.

Additionally, developing public-private partnerships could foster innovative solutions to support financial stability in the real estate sector. For instance, governments can consider offering tax incentives for adaptive reuse projects or implementing policies that encourage sustainable development practices. By leveraging both public initiatives and private sector capabilities, policymakers and industry leaders can collaboratively create a more resilient commercial real estate framework and ultimately mitigate the effects of high vacancy rates and rising interest rates.

Preparing for Potential Bad Debt and Defaults

With many commercial real estate loans maturing soon, the potential for defaults raises alarm bells. Financial institutions, particularly regional banks that may be more susceptible to downturns, must prepare for the possibility of increased bad debt. Proactive measures such as revisiting lending practices and ensuring prudent risk assessments are essential to mitigate the impacts of delinquent loans. By strengthening their financial cushions and enhancing liquidity, banks can fortify themselves against the impending wave of commercial real estate challenges.

Moreover, maintaining open lines of communication with borrowers can also facilitate more effective resolutions. Engaging collaboratively with distressed clients—offering restructuring options or exploring alternative financing solutions—can help mitigate losses while fostering a recovery environment. Fully addressing the depth of bad debt risk is critical to maintaining overall financial stability, as these measures can buffer against widespread financial contagion that may stem from the commercial real estate crisis.

The Future Outlook for Commercial Real Estate

Looking ahead, the future of commercial real estate is fraught with uncertainty but is not devoid of opportunity. While current projections suggest high vacancy rates and increased risks could linger in the short term, evolving consumer preferences may drive changes that reshape the market landscape. Investors who can pivot quickly and adapt to these shifts may find new opportunities for growth, particularly in sectors that emphasize sustainability and flexibility, responding to changes in workplace dynamics post-pandemic.

Ultimately, the trajectory of commercial real estate will hinge on various factors, including interest rates, economic health, and broader societal trends. Stakeholders must remain vigilant, prepared to reassess traditional business models and embrace innovative solutions that cater to the changing needs of tenants and the market. As the sector confronts these multifaceted challenges, maintaining a proactive and adaptable mindset will be key to navigating the path forward.

Frequently Asked Questions

How are high office vacancy rates contributing to the commercial real estate crisis?

High office vacancy rates, which currently range from 12% to 23% in major U.S. cities, are negatively impacting the commercial real estate crisis by depressing property values and increasing the risk of delinquencies on real estate loans. With demand for office space declining due to changes in work habits post-pandemic, investors are facing significant losses, which could lead to further economic instability.

What impact do interest rates have on the commercial real estate crisis?

The impact of interest rates on the commercial real estate crisis is profound. As interest rates remain high, property owners may struggle to refinance their real estate loans, leading to increased defaults. This situation can cause localized pain in the banking system, particularly among regional banks that are heavily invested in commercial real estate.

Can the vulnerabilities in the banking system exacerbate the commercial real estate crisis?

Yes, vulnerabilities in the banking system can exacerbate the commercial real estate crisis. If regional banks, which may be more susceptible to losses from delinquent commercial real estate loans, experience failures, it could create a domino effect impacting credit availability and economic stability sector-wide.

What are the economic implications of the commercial real estate crisis?

The economic implications of the commercial real estate crisis include potential losses in pension funds, tighter lending conditions, and reduced consumer spending. While the overall economy may not be severely affected at this time, ongoing challenges in the commercial real estate sector could lead to broader economic repercussions if not addressed.

How can rising delinquency rates on commercial real estate loans affect consumers?

Rising delinquency rates on commercial real estate loans can indirectly affect consumers by leading to stricter lending conditions from banks, which in turn can reduce availability of credit and impact consumer spending. Local economies heavily reliant on regional banks may experience localized downturns as well.

| Key Point | Description |

|---|---|

| High Office Vacancy Rates | Office space demand has decreased significantly post-pandemic, with vacancy rates in major cities ranging from 12% to 23%. |

| Impact on Property Values | Plummeting demand has lowered property values, raising concerns among financial experts about potential bank losses. |

| Commercial Mortgage Debt | 20% of the $4.7 trillion in commercial mortgage debt is due this year, posing risks to lenders and financial markets. |

| Bank Stability Concerns | While large banks are better regulated and diversified, some smaller banks might struggle with the impending debt crisis. |

| Future Predictions | Experts predict that long-term interest rates will remain stable, complicating the financing environment for commercial real estate. |

| Consumer Impact | Local economies could suffer due to regional bank losses, but strong job and stock markets may cushion the effects. |

Summary

The commercial real estate crisis poses significant challenges to the economy as rising vacancy rates and maturing debt threaten financial stability. With demand for office spaces plummeting and major banks facing potential losses, experts warn that this could lead to a ripple effect, impacting regional banks and the broader economic landscape. The situation demands careful monitoring, as the success of regional economies may hinge on the resolution of these commercial real estate issues.